July 13, 2026

The Week Ahead

Cotton enters the week looking for its next catalyst, with weather, Tuesday’s CPI report, and the ongoing conflict in the Middle East expected to influence outside market direction.

- Tuesday’s CPI report will be the biggest macro event this week. A softer-than-expected inflation reading could weigh on the U.S. dollar and provide support across commodity markets, while a stronger reading would likely have the opposite effect. Thursday’s Retail Sales report will offer another look at the strength of the U.S. economy and could also influence outside market direction.

- Renewed tensions between the U.S. and Iran brought geopolitical risk back into the market after both countries exchanged additional strikes over the weekend. To start the week, President Trump said the U.S. will reinstate the blockade on the Strait of Hormuz and proposed a 20% reimbursement fee on cargo moving through the Strait, adding another headline for markets to digest as the week gets underway.

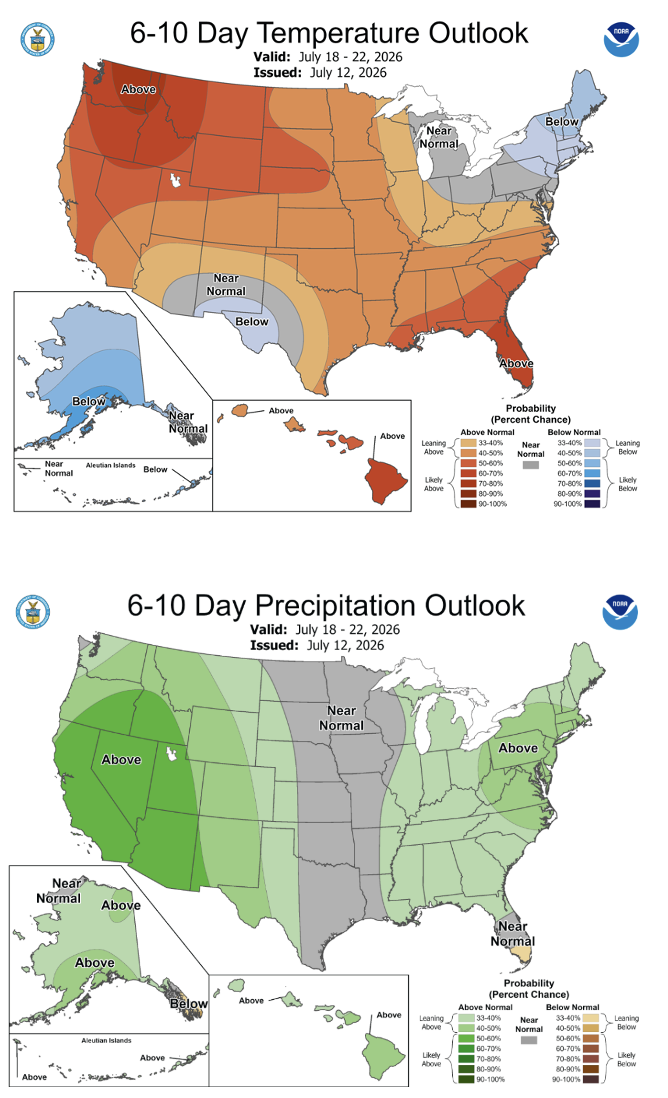

- Weather will remain one of the market’s biggest drivers, but last week showed that cotton isn’t trading on weather alone. Beneficial rainfall fell across much of the Cotton Belt, yet futures still moved higher as speculative buying and technical momentum outweighed the improving forecast. If weather concerns begin to ease, funds may become less aggressive buyers, making weather forecasts and speculative positioning even more important over the next few weeks.

- Attention will also turn to Thursday’s Export Sales Report and Friday’s CFTC Commitments of Traders report. Export sales will provide another look at demand, while the CFTC report will show whether funds continued adding to long positions after returning as net buyers last week.

Market Recap

Market Recap

- Cotton futures posted a strong week as weather concerns, outside markets, and speculative buying all helped support prices. Trading wasn’t one-sided, though, as the market responded to several headlines throughout the week. December futures settled at 81.54 cents per pound, up 442 points on the week.

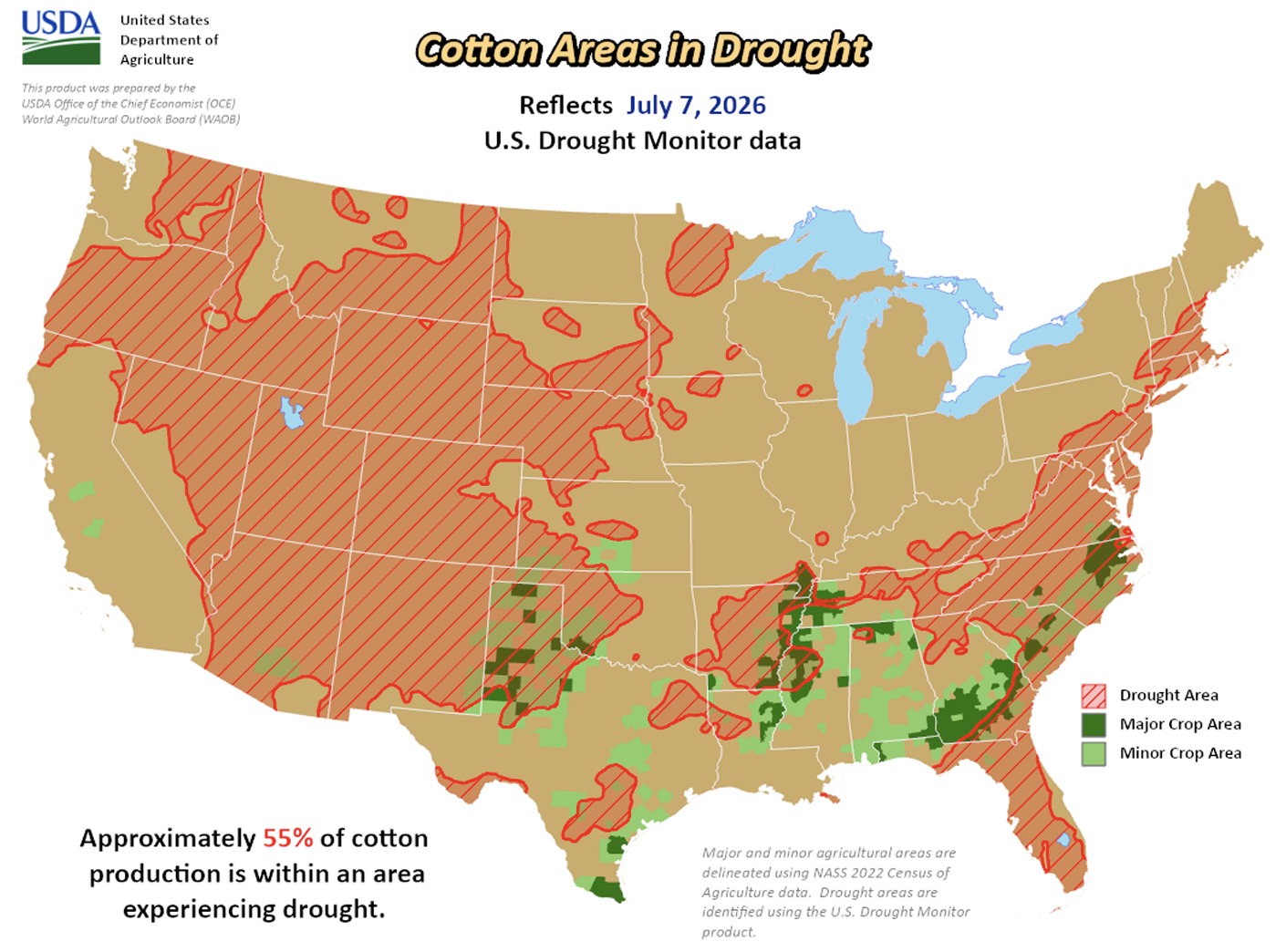

- The rally got started after U.S. crop conditions declined for the third straight week and forecasts called for hot, dry weather across parts of the Cotton Belt. At the same time, renewed tensions in the Middle East pushed crude oil prices higher, while optimism surrounding potential U.S.-China trade discussions spilled over into the broader agricultural markets. Together, those factors helped bring buyers back into cotton and kept prices well supported through the first half of the week.

- By Thursday, most of the market’s attention had shifted to USDA reports. Export sales offered little excitement, while Friday’s WASDE increased both U.S. production and ending stocks. Even so, the market’s reaction was fairly short-lived. Futures initially moved lower after the report but quickly recovered as buyers stepped back in, suggesting traders had largely expected the larger crop.

- Another supportive factor was the return of speculative buying. Managed money came back as net buyers after several weeks of selling, while technical buying picked up as December futures pushed through key resistance levels. With weather still front and center and funds becoming more active, the market heads into next week with a much different tone than it had just a few weeks ago.

Economic and Policy Outlook

Economic and Policy Outlook

- USDA recently finalized several changes to the Marketing Assistance Loan (MAL) program through the One Big Beautiful Bill Act. As a reminder, most notably for cotton, the upland loan rate increased from 52 to 55 cents per pound beginning with the 2026 crop, along with several updates to the adjusted world price calculation and loan repayment provisions.

- Geopolitical concerns moved back into focus over the weekend after the U.S. and Iran exchanged additional strikes. Uncertainty surrounding the Strait of Hormuz pushed crude oil prices higher as traders weighed the potential for disruptions to global energy supplies. Higher crude prices provided outside support to cotton, although weather and speculative buying remained the market’s primary drivers.

- Minutes from the Federal Reserve’s June meeting showed policymakers remain concerned about inflation, with a few officials believing there was a case for raising interest rates before ultimately voting to leave rates unchanged. Markets continue to expect one to two rate hikes this year, with Tuesday’s CPI report expected to provide the next major clue on the Fed’s path forward.

Supply and Demand Overview

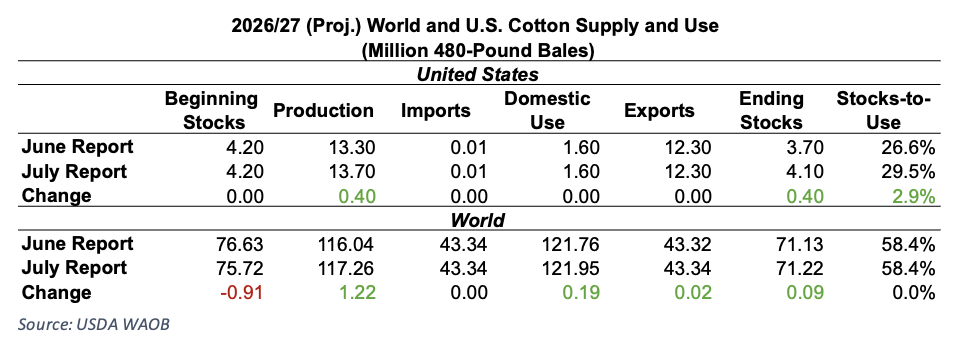

- This past Friday’s USDA WASDE report was slightly bearish for cotton, although the changes were largely expected following the June Acreage report. USDA increased U.S. production by 400,000 bales to 13.7 million, reflecting higher planted acreage and a small increase in yield. With no changes to domestic use or exports, ending stocks also increased by 400,000 bales to 4.1 million bales.

- On the global side, USDA raised world production by 1.2 million bales to 117.3 million, with larger crops expected in the United States, Brazil, Turkey, and Central Asia. World mill use increased only slightly, while exports were essentially unchanged. As a result, 2026/27 world ending stocks increased modestly to 71.2 million bales. Despite the higher ending stocks, demand is outpacing production for the first time since the 2023 crop year.

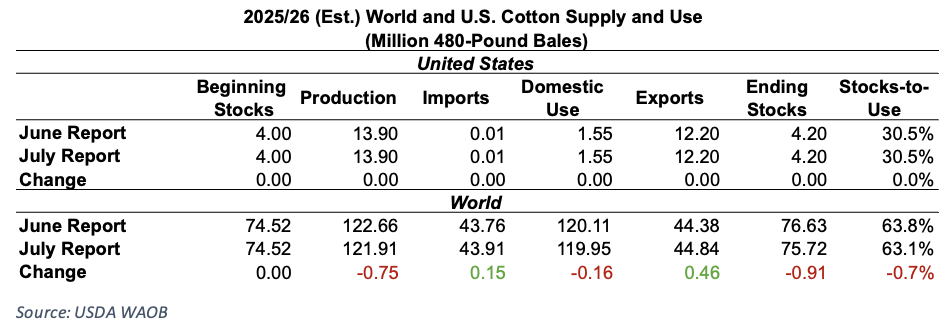

- USDA made only minor adjustments to the 2025/26 balance sheet. U.S. supply and demand estimates were left unchanged. Globally, production and ending stocks were reduced, largely because of a smaller Brazilian crop, while exports increased slightly.

- Overall, this past week’s Export Sales Report was mixed. Upland sales totaled 66,400 bales for the current marketing year, up 36% from the previous week but still 49% below the four-week average. Vietnam and India led buying activity, followed by Mexico, Bangladesh, and China. New crop sales improved to 87,000 bales, with Vietnam and Turkey accounting for most of the total.

- Upland exports reached 230,100 bales, up 5% from the previous week but 14% below the four-week average. Vietnam was the top destination, followed by Pakistan, Turkey, Bangladesh, and Mexico.

- With only a few weeks left in the marketing year, shipments will need to pick up to reach USDA’s 12.2 million bale export forecast.

- Pima sales increased to 2,600 bales, while new crop sales totaled 17,500 bales, all to India. Pima exports fell to 10,600 bales, down 57% from the previous week and 38% below the four-week average.

The Seam®

The Seam®

- As of Thursday afternoon, grower offers totaled 1,354 bales. The past week, 242 bales traded on the G2B platform received an average price of 68.15 cents per pound. The average loan redemption rate (LRR) was 53.03, bringing the average premium over the LRR to 15.12 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).