The textile industry has struggled to recover after reaching its high in the 2021/22 crop season.

by Abigail Hoelscher

The Uyghur Forced Labor Prevention Act

The Uyghur Forced Labor Prevention Act (UFLPA) was enacted almost two years ago to ensure the integrity of the textile industry and what kind of apparel and garments enter the U.S. This act forced the retail industry to guarantee that the cotton used in their products does not originate from regions where forced labor practices actively occur. It also forced many brands and retailers to evaluate and comply with the standards. Since UFLPA was enacted, the U.S. has detained over $55.92 million worth of apparel, footwear, and textiles imported from other countries.

The Xinjiang region in China specifically accounted for 90% of the country’s cotton output. A large portion of China’s exports of yarn, fabric, and garments are from this region. As a result of non-compliance with the UFLPA rules, goods manufactured wholly or in part from this region are prohibited from entering the United States. The landscape of the textile industry has changed as many manufacturers receive yarn and fabric from China. The new laws have impacted the industry, and now traceable cotton will take the forefront of the global supply chain to ensure proof of origin and UFLPA compliance.

Supply Shortage

Unsurprisingly, a supply shortage in the U.S. has added pressure to the recovering textile industry over the past two years. The U.S. leads the world with cotton exports, but the past two short crops have led to a lower-than-average amount of cotton leaving the country for foreign mill use. As mentioned above, the U.S. has stricter laws on cotton products entering the country. Being a leader in traceable cotton has impacted the amount of cotton used across the globe because of the shorter crops. Cotton consumption has been unstable since the Covid-19 pandemic. One of the biggest causes of instability has been the economic outlook of global inflation and the cycle of rising interest rates. After the 2021/22 high, a potential economic downturn began to worry many involved in the textile industry, and inventories began to fall and remained low as the industry tried to keep risk down.

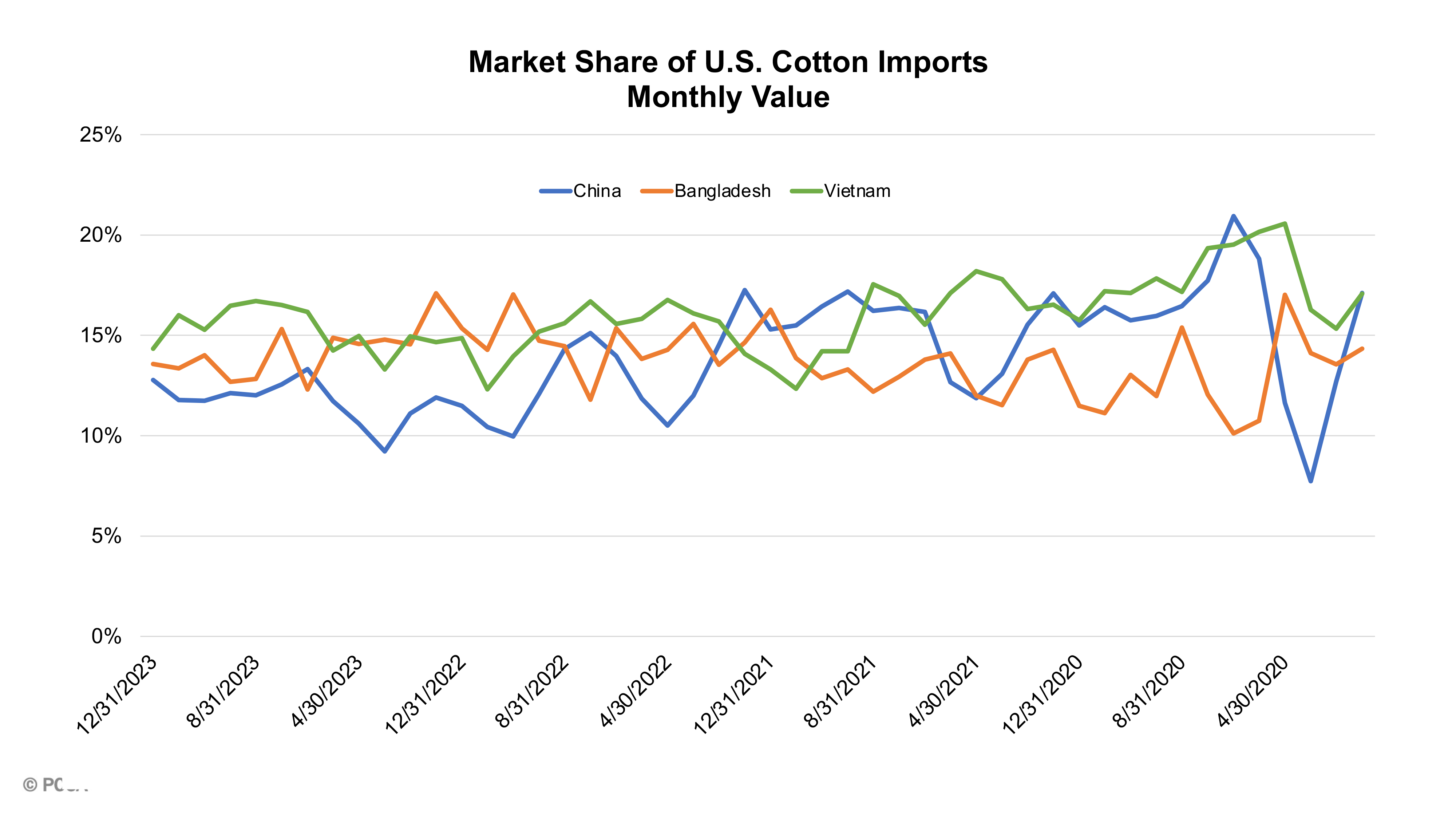

China, Bangladesh, and Vietnam make up 41% of the current value of U.S. cotton exports. After the COVID-19 recovery, another dip occurred in these countries as UFLPA was enacted, and the global economy fell under pressure. The amount of cotton going to these countries has started to recover, but it has been slow. Data Source: The Office of Textiles and Apparel (OTEXA)

Competition

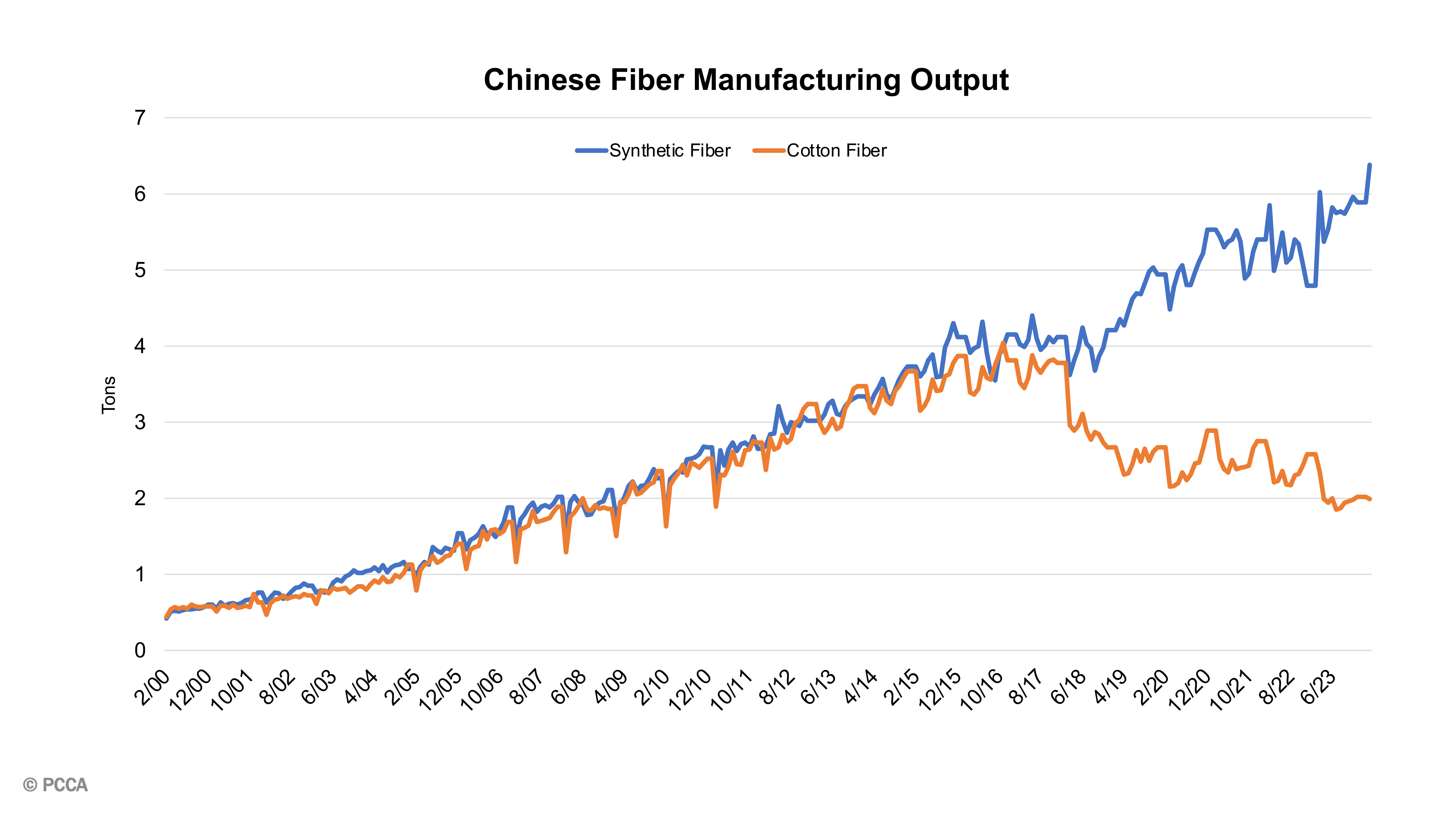

The textile industry must also compete with man-made fibers. On a global scale, overall man-made fiber production and consumption have steadily increased since the 1990s. However, cotton production has remained relatively stable during that time. Synthetic fibers account for a larger share of U.S. imports in recent years as they are typically more cost-efficient to manufacture than growing and processing natural fiber. The ability to rapidly produce large quantities of clothes at an inexpensive price has made it harder for natural fibers to compete. China produces most of the world’s synthetic fibers and output of synthetics is now over three times that of cotton. A larger crop could help cotton reclaim a portion of the market share lost to man-made fibers due to more competitively priced cotton.

China is the largest manufacturer and producer of synthetic fibers, producing about 72% of the world’s synthetics and exporting approximately 45% of the produced fibers. There has been a divergence in the synthetic fiber leaving the country compared to cotton fiber in the last six years. Data source: Bloomberg Chart generated: PCCA

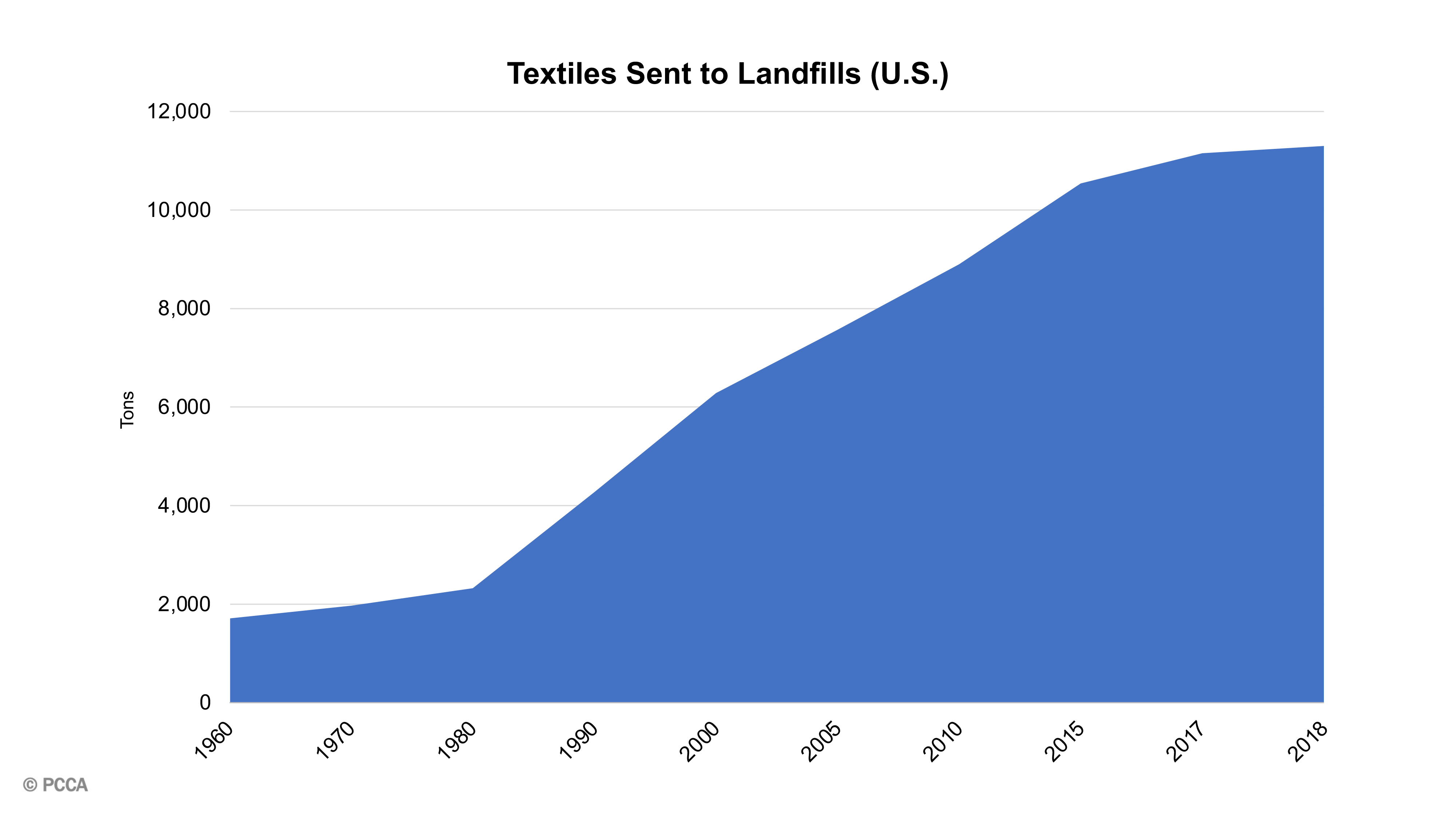

The rapid production of synthetics and increased purchasing of fast fashion has caused a rise in textiles sent to landfills. Synthetic fibers biodegrade much slower than cotton. Cotton fibers break down naturally, similiar to food and plants. Data source: epa.gov Chart generated: PCCA

The textile industry has faced a perfect storm of problems in the past few years. There does seem to be a light at the end of the tunnel for the upcoming crop. Becoming familiar with the laws of UFLPA has made the industry more conscious of where cotton is sourced from. The U.S. is a leader in the traceability of cotton, which stands to continue in the upcoming season. U.S. production is expected to rebound, and cotton consumption is projected to rise to its highest level since 2021. While there is always a possibility of negative factors that could impact production and consumption in 2024/25, the current outlook for cotton consumption appears positive.