By Abigail Hoelscher

A Landscape of Uncertainty

I asked my AI platform to count the number of news stories with the word “uncertainty” in 2025. The platform said there are so many that it was “effectively impossible” to know. Yet, it’s a word that remains the most accurate way to describe the current global landscape. While the future of trade policy was unclear under a new administration, it was evident that significant changes were on the horizon. Although all sectors are exposed to this uncertainty, global commodity markets, particularly those of cotton, are especially vulnerable to the resulting volatility.

Tariffs and Market Volatility

Tariffs and Market Volatility

Tariffs function like trade taxes, raising the cost of moving goods across borders. When a major buyer or seller imposes tariffs, trade flows shift, disrupting established supply chains. Although tariffs are not new, their recent application has caused significant market concern as affected countries scramble to find new buyers. Over the past six months, the United States has imposed numerous tariffs on countries that import U.S. cotton, resulting in an excess supply and dampened demand, which has kept prices within a narrow, low trading range.

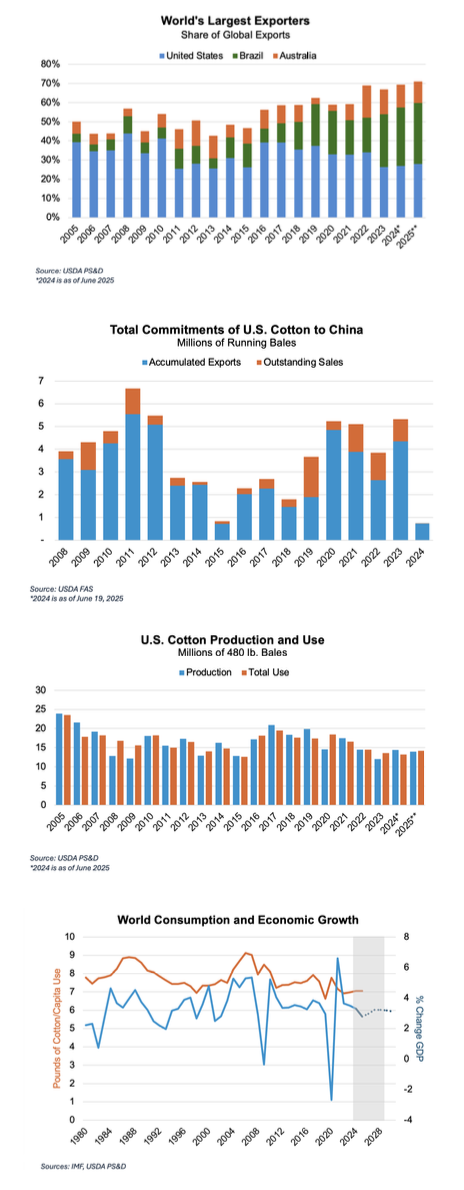

This is not the first time cotton has been caught in the crossfire of trade tensions. The 2018/19 U.S.-China trade war severely impacted U.S. cotton producers, as China, historically the largest buyer of U.S. cotton, dramatically reduced imports following the imposition of U.S. tariffs on Chinese goods.

Meanwhile, global cotton production from competitors surged to fill China’s needs, with Brazilian production and exports expanding sharply, and Australia consistently delivering large crops over the past four years. Together, these shifts have eroded U.S. market share and heightened challenges for U.S. cotton exporters.

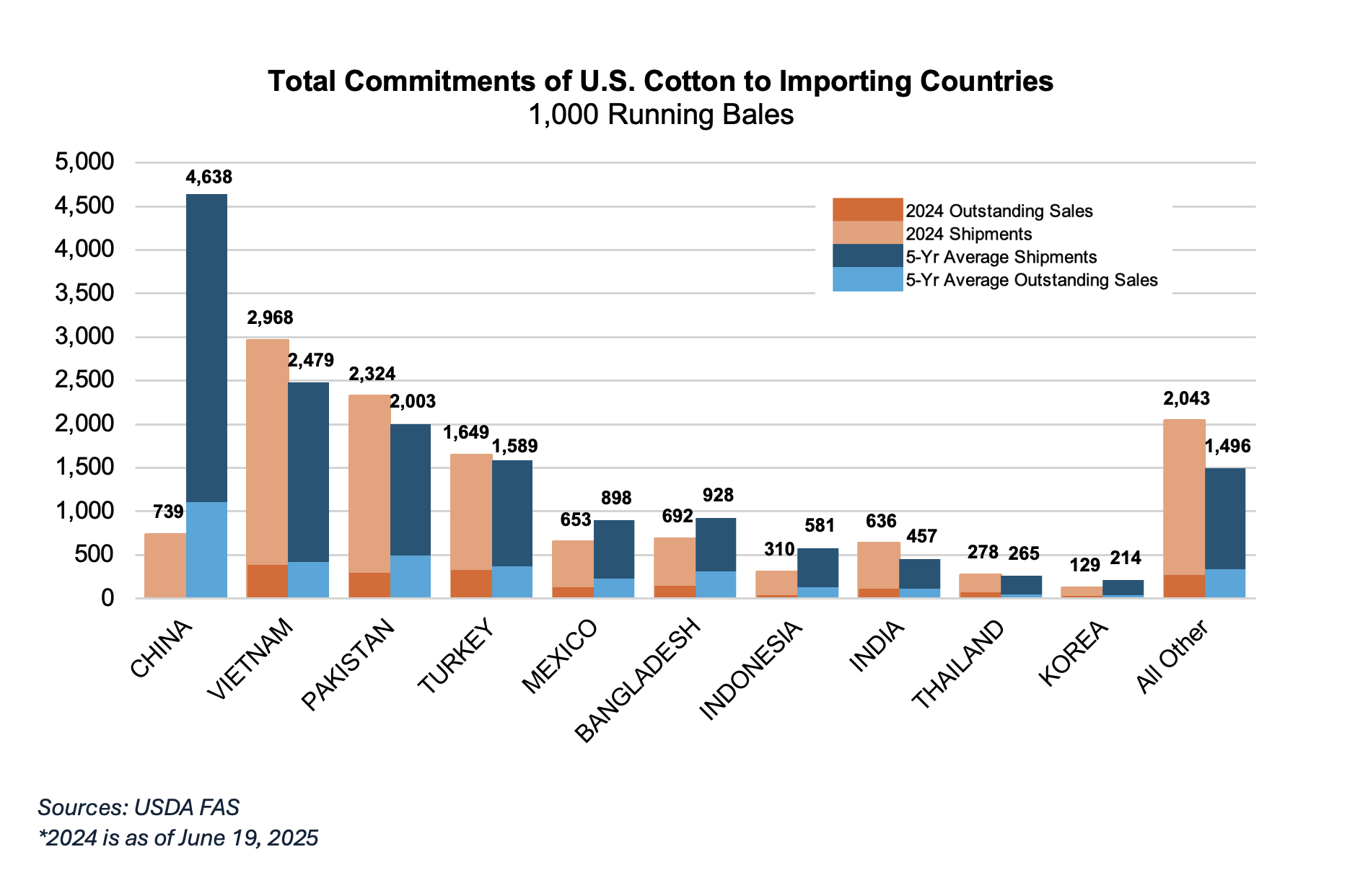

In the 2024/25 season, China has remained notably absent from the U.S. cotton market, and projections indicate a similar trend for the 2025/26 season. China’s substantial purchases during the 2023/24 season were likely made in anticipation of potential trade volatility under a new administration. Markets dislike volatility, and tariffs disrupt supply chains from farmers to traders to consumers. Although other buyers have stepped in, China’s absence is significant in the global landscape.

Moreover, the slower-than-expected growth in global cotton use underscores that trade wars rarely produce winners. In an interconnected world, stable trade is essential. U.S. cotton, known for its quality and scale, remains critical to global textile manufacturing. Policies that promote stable, fair trade ensure this natural fiber can reach markets without unnecessary barriers. The recent turbulence highlights the importance of cooperation over confrontation.

Supply and Demand Outlook

Looking ahead, several factors could help support U.S. cotton demand, though uncertainty remains high. As of this writing, USDA projects 2025/26 U.S. production at 14 million bales, with exports expected to reach 12.5 million bales, an increase from the year prior. While carryover stocks from the 2024 crop remain a concern, they are not as burdensome as feared thanks to strong export shipments. Early worries about a potential surplus in 2025/26 raised questions about global demand, but those concerns have eased somewhat as export projections have held steady and production estimates have declined.

Still, while global consumption is projected at 117.76 million bales, many in the trade remain skeptical that demand will reach those levels given ongoing market headwinds. Trade agreements are crucial for boosting cotton consumption. Markets need clarity and direction; without it, prices will remain under pressure. The initial tariffs imposed by President Trump were broad-based, with a 10% rate on most imports and higher rates for countries with significant trade surpluses. Many of these countries were major importers of U.S. cotton, which shook the market upon the announcement. Though some country-specific tariffs were temporarily paused, China’s tariffs remained high. Subsequent negotiations led to a partial rollback—U.S. tariffs fell from 145% to 30%, while China reduced its tariffs from 125% to 10%.

The current Chinese tariff rate on U.S. cotton is 10%, but it was as high as 15% at one point. As of this writing, the tariffs have been temporarily paused, with suspensions expiring in July for some countries and August for others. Yet the path forward is still uncertain, and greater clarity wouldhelp reduce market volatility. Recently, Senator Cindy Hyde-Smith introduced the

“Buying American Cotton Act,” which proposes a transferable tax credit for end-stage sellers of products made wholly or partly from U.S. cotton. This credit would apply to both domestically produced and imported goods containing verified U.S.-grown cotton. Though still awaiting a Congressional Budget Office score, the bill has attracted bipartisan support, a promising sign for the industry.

Meanwhile, India plans to raise its Minimum Support Price (MSP) for the 2025/26 season by 8%, well above market expectations of 3–4%. This move could boost Indian cotton prices, potentially making U.S. cotton more competitive in global markets through higher import parity. Higher MSPs may incentivize Indian mills to seek more affordable foreign cotton. Depending on exchange rates, this implies prices for Indian cotton would be between 92 and 95 cents per pound after the cotton has been ginned, though actual cash prices can trade below MSP as they have historically. A stronger Indian rupee would push prices higher in U.S. dollar terms, while a weaker rupee would have the opposite effect.

A potential global recession poses another risk to the cotton market. A downturn would reduce consumers’ discretionary spending, impacting demand for clothing and other cotton-based products. Lower demand would push prices down, exacerbating a challenge the industry already faces. Consumers would also be more inclined to purchase cheaper goods, which could allow man-made fibers to capture a greater market share from natural fibers. Rising production costs could make cotton farming less attractive, further pressuring supply. Recession-driven demand destruction would deepen the imbalance between supply and demand, further intensifying price pressures.

Navigating an Uncertain Future

The post-COVID years have been detrimental to the demand for cotton. Growth has been slow, while prices and policies have been volatile. Despite the challenges, U.S. cotton remains vital to the supply chain thanks to its dependable quality and global reputation. As more trade certainty emerges, market direction will become clearer. Until then, the industry must continue to navigate uncertainty and persevere through challenging times.