May 11, 2026

The Week Ahead

Macro headlines are expected to drive the market this week, with talks involving Iran back in focus, a meeting with China on deck, and a busy slate of economic and fundamental data ahead.

- Macro headlines will stay in the driver’s seat this week, with CPI inflation, the May WASDE report, and the Trump-Xi summit all ahead. Outside markets turned a little more supportive late last week as the dollar weakened and equities pushed back to new highs, but a hotter inflation number could quickly shift the tone and weigh on export-driven commodities like cotton.

- Energy remains an important part of the story, with crude oil continuing to react to U.S.-Iran developments. Higher crude prices would likely keep supporting the broader commodity space and increasing the cost of polyester, cotton’s primary competitor.

- For cotton, positioning and seasonals are becoming more important. Funds are still carrying a sizeable long across agriculture, including cotton, leaving the market a little more vulnerable if outside support starts to fade or if upcoming data disappoints.

- Tuesday’s WASDE report will be the main fundamental focus of the week, giving the market its first official look at the 2026/27 balance sheet. Attention will be on production estimates, export demand, global consumption, and how USDA handles the early weather outlook heading into the growing season.

Market Recap

Market Recap

- Cotton futures saw another volatile week, with July trading in a wide range before settling at 84.73 cents per pound, up 54 points for the week. The December contract was up 90 points at 85.46 cents.

- Much of the week’s price action continued to follow outside markets, particularly crude oil, as headlines tied to U.S.-Iran negotiations and the Strait of Hormuz drove sharp swings across the broader commodity space. Even with periods of “risk-off” pressure tied to weaker crude and softer equities, cotton continued to hold near contract highs and maintained a supportive technical tone overall.

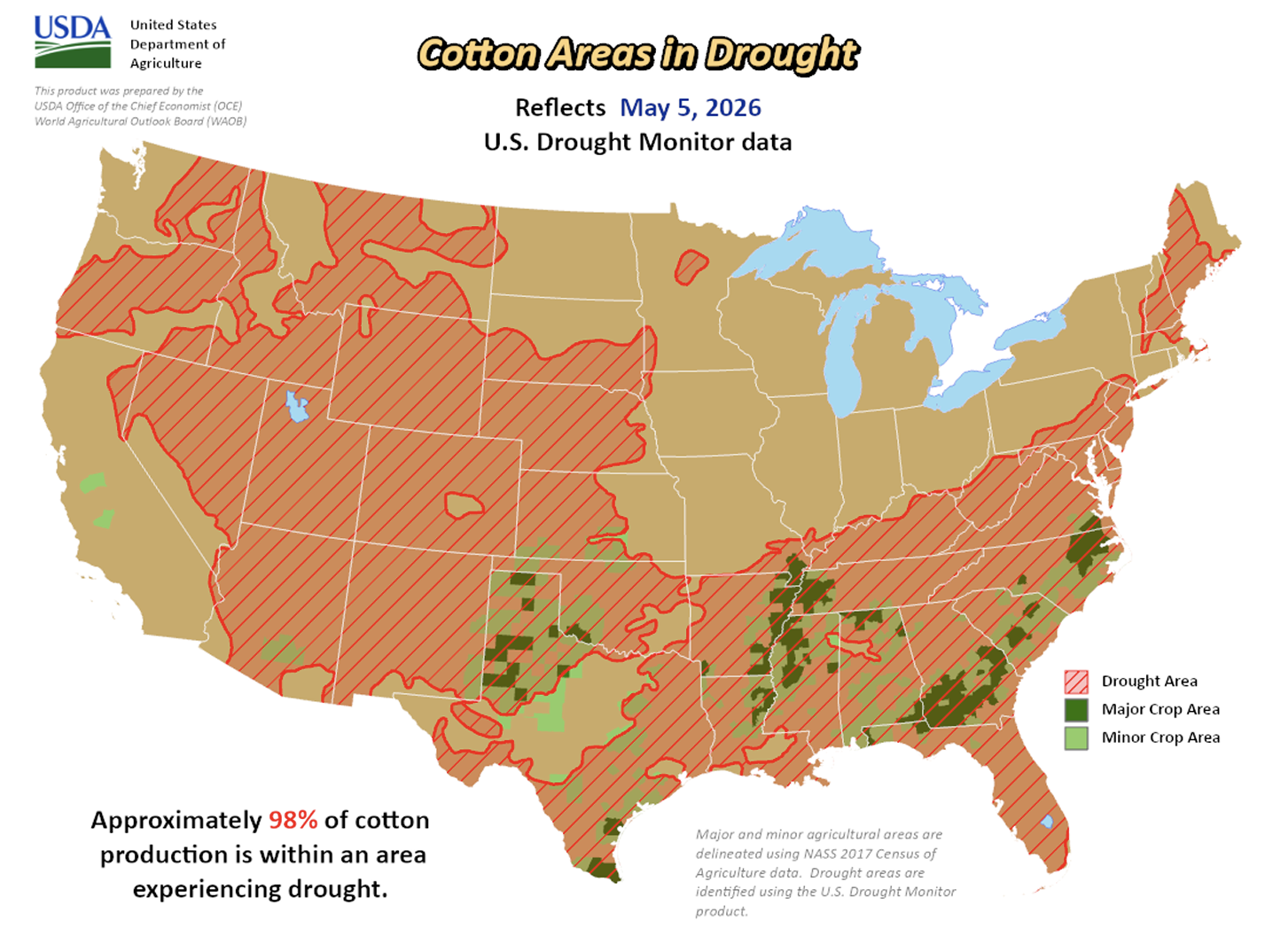

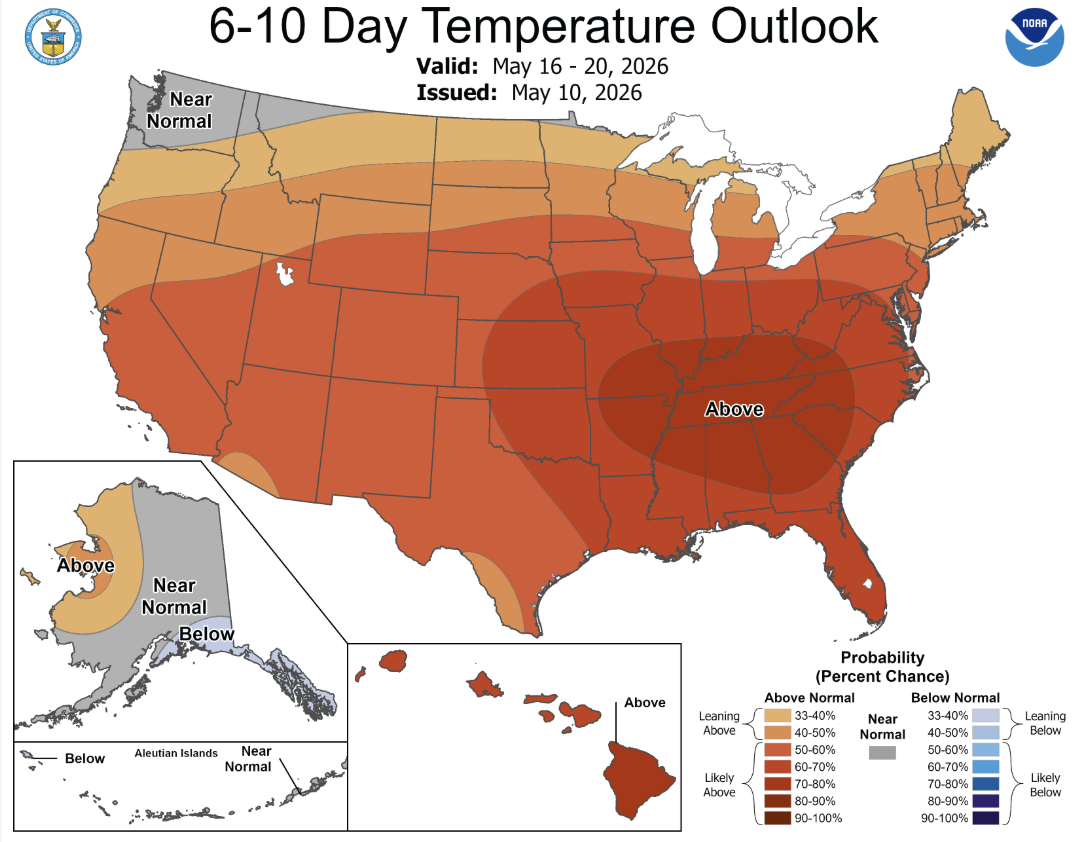

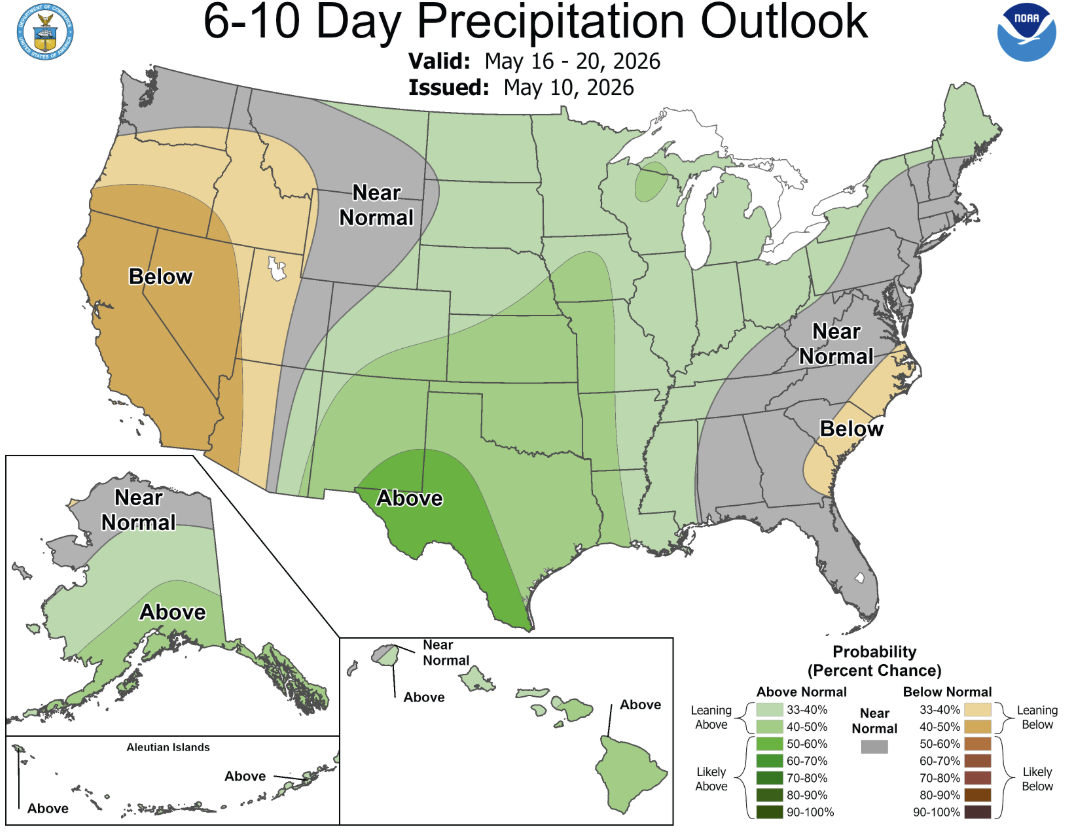

- Fundamentally, export sales softened some as higher prices appeared to slow demand, though shipments remained strong and continue running ahead of the pace needed to meet USDA’s current export projection. Weather remained in focus as well, with beneficial rainfall across parts of the Delta and Southeast while much of West Texas stayed mostly dry. Planting progress remains near to slightly ahead of average despite drought conditions still covering most of the Cotton Belt.

- Looking at the overall position, speculative buying continued to support the market, though the pace has started to slow compared to earlier in the rally. Funds are heavily long agriculture, while stocks deliverable against futures continued building through the week, and on-call data showed the old-crop imbalance narrowing modestly.

Economic and Policy Outlook

Economic and Policy Outlook

- China officially confirmed President Trump’s May 13–15 visit to meet with President Xi Jinping in Beijing, marking the first U.S. presidential trip to China in nearly a decade after earlier delays tied to the Iran conflict. Markets are hoping for signs of easing trade tensions, potential agricultural purchase agreements, and discussions surrounding energy flows, tariffs, and rare-earth exports.

- Iran and the U.S. continued ceasefire discussions this week, with Iran formally responding to the latest proposal and signaling a willingness to focus initial talks on halting hostilities and reopening shipping through the Strait of Hormuz rather than addressing broader disputes. The negotiations appear aimed more at stabilizing energy flows and reducing regional escalation than at reaching a broader peace agreement, as disruptions in the Gulf continue to impact global energy and shipping markets. President Trump later warned Iran against “playing games” after reports the two sides remain far apart on several key issues.

- On that note, the Senate Ag Committee will hold a hearing on Tuesday, May 12, focused on fertilizer affordability and supply stability, as prices remain elevated following disruptions tied to the Iran conflict and ongoing concerns about shipping through the Strait of Hormuz.

- A U.S. trade court ruled that the Trump administration’s latest 10% temporary global tariffs were not justified under Section 122, marking another legal setback for the administration’s tariff strategy. While the ruling only blocks the tariffs for a small group of importers for now, CBP is reportedly preparing to begin processing tariff refunds tied to earlier court rulings, with billions in potential repayments expected across industries, including agriculture. Markets will also be watching whether the administration shifts toward broader Section 301 tariffs later this year.

Supply and Demand Overview

- U.S. export sales softened in the most recent report, with net upland sales totaling 123,300 bales for the current marketing year, down from both the previous week and the recent average. Pakistan, India, and Vietnam led buying, with additional support from Indonesia and Bangladesh. New crop sales came in at 48,400 bales, led primarily by Guatemala and Indonesia, while some reductions to Vietnam weighed on totals.

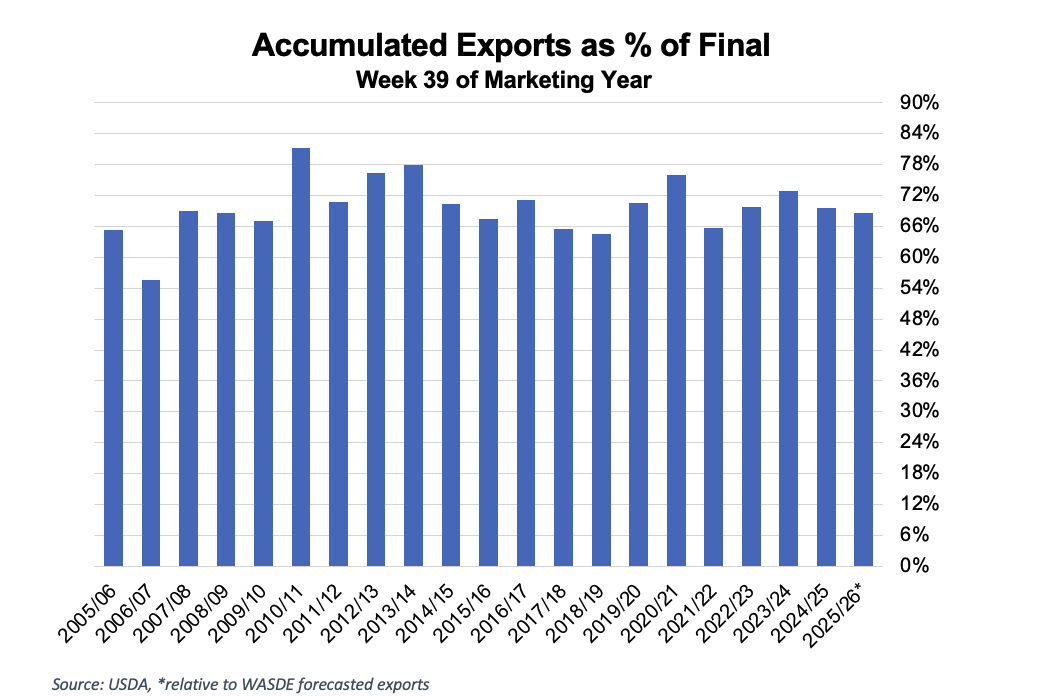

- Shipments remained solid at 327,500 bales, though they eased from the previous week. Vietnam was again the top destination, followed by Bangladesh, Pakistan, Turkey, and China. Pima sales also slowed to 11,500 bales, while shipments totaled 14,800 bales. Even with some moderation in sales activity as prices remain elevated, shipments continue to run ahead of the pace needed to meet USDA’s current 12 million-bale export projection if maintained.

The Seam®

The Seam®

- As of Friday afternoon, grower offers totaled 16,238 bales. The past week, 3,324 bales traded on the G2B platform received an average price of 75.36 cents per pound. The average loan redemption rate (LRR) was 53.62, bringing the average premium over the LRR to 21.74 cents per pound.

Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Sustainability Enrollment Opportunities

Sustainability Enrollment Opportunities

- New Grower Enrollment for the Better Cotton Initiative will be open from March 3 to May 30. Growers interested in joining this global sustainability program should contact PCCA (806) 763-8011.