July 27, 2026

The Week Ahead

- Cotton begins the week with attention centered on Wednesday’s Federal Reserve meeting, while traders also keep an eye on weather, export demand, and developments in Washington that could affect agricultural policy.

- Wednesday’s Federal Reserve meeting will be the biggest event of the week. While no change in interest rates is expected, traders will be paying close attention to Chair Warsh’s comments for clues about the path of monetary policy. Any indication the Fed plans to keep rates higher for longer could lend support to the U.S. dollar and weigh on commodity markets, including cotton.

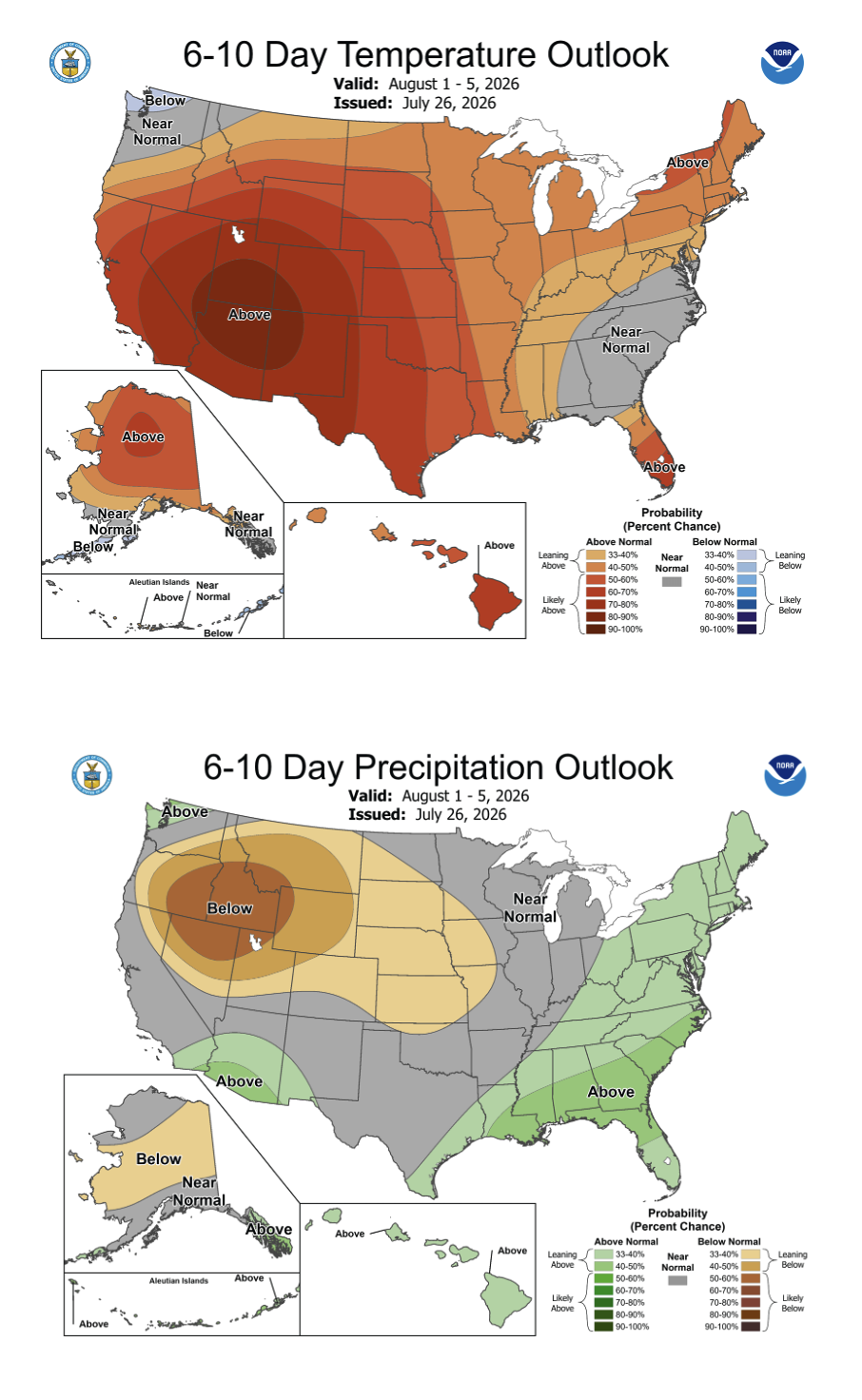

- Weather will stay front and center as the U.S. crop moves through a key stage of development. Hot temperatures are expected across much of the Cotton Belt early in the week, with scattered chances for rain later on. Forecast changes, especially across West Texas, are likely to keep weather premium in the market.

- Washington could also draw some attention as the Senate works through several agriculture priorities before its August recess, including discussions surrounding the Farm Bill and a proposal for additional producer assistance. While there are still plenty of hurdles to clear, any progress could be meaningful for agriculture heading into the fall.

- Thursday’s Export Sales Report will provide another look at demand, while Friday’s CFTC Commitments of Traders report will show whether funds kept adding to their positions after several weeks of buying.

Market Recap

- Cotton futures traded mostly higher this past week as weather concerns and strength in outside markets helped offset lingering demand concerns. December futures settled at 79.98 cents per pound, up 135 points on the week.

- Early in the week, traders sorted through several supportive headlines. China’s reserve auctions remained well subscribed, crude oil moved higher following renewed tensions in the Middle East, and hot, dry weather across portions of West Texas added some weather premium back into the market. By the end of the week, scattered rainfall reached parts of the Cotton Belt, limiting further gains, though forecasts remained mixed and weather stayed at the forefront of the market.

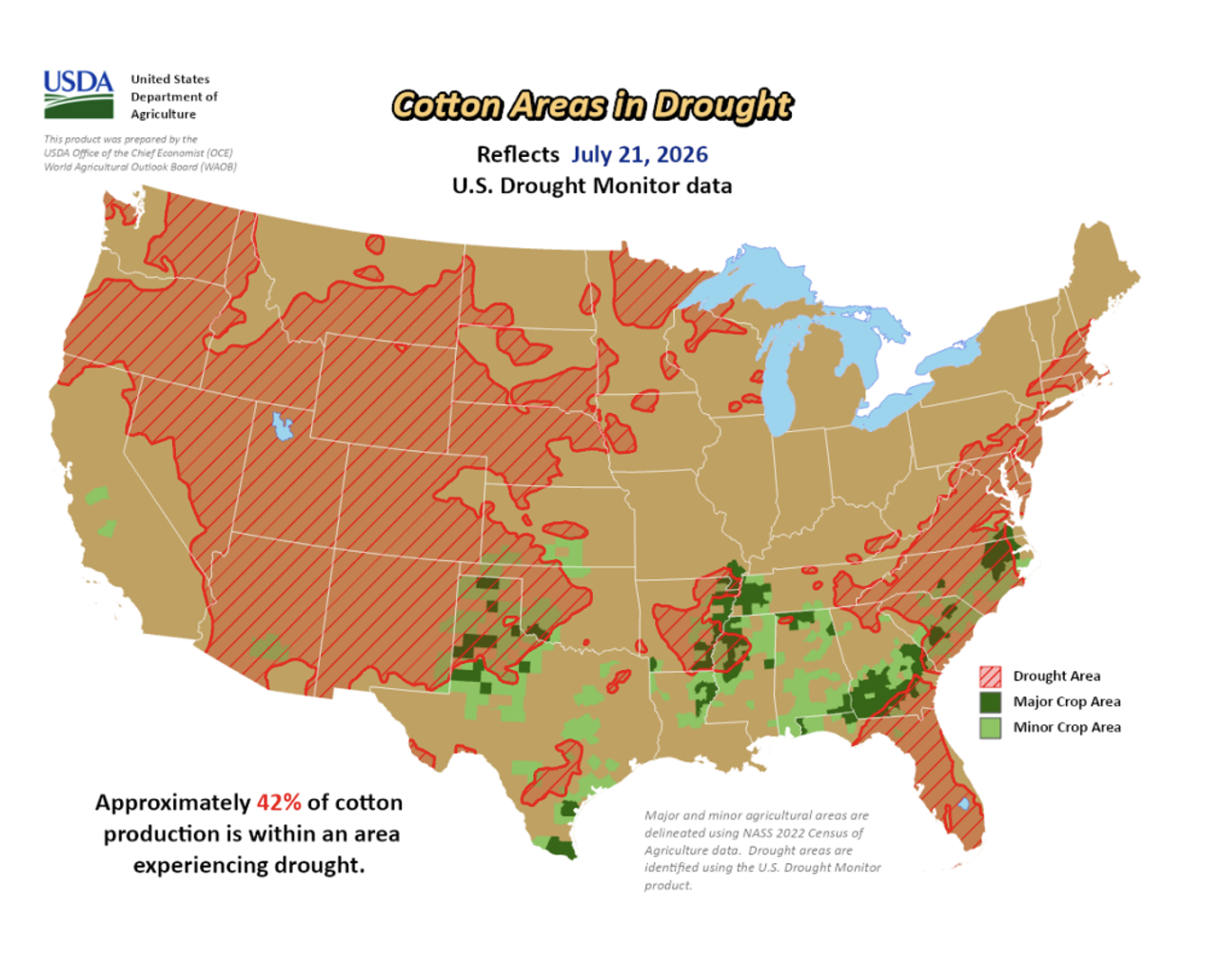

- The latest U.S. Drought Monitor showed the share of cotton acreage experiencing drought declined from 46% to 42%. Even so, crop conditions remain mixed across the Cotton Belt, with some areas benefiting from timely rainfall while others continue to struggle with heat and limited moisture. As the crop enters a critical stage of development, another round of triple-digit temperatures is expected across West Texas. Recent rainfall has improved conditions in some areas, but the crop remains highly variable, and weather over the next week will be important in determining yield potential, especially for dryland acres.

- Friday’s Commitments of Traders report showed managed money added to its net long position for another week, while index funds were also net buyers. Positioning remains supportive, although trading activity has started to slow as the market moves through the late-summer period.

Economic and Policy Outlook

- Geopolitical tensions remained a key focus last week, though the tone shifted over the weekend as the U.S. and Iran paused military strikes for a second straight day. The pause came as Iranian and Omani officials resumed talks aimed at restoring shipping through the Strait of Hormuz, easing some concerns over potential energy supply disruptions. Crude oil prices fell sharply on the news after briefly trading above $100 per barrel last week. While the situation remains fluid and the U.S. has indicated all options are still on the table, traders will continue watching developments in the Middle East for any signs that tensions could escalate again and impact energy markets.

- The U.S. Trade Representative officially announced Section 301 tariffs on 60 economies, with rates of 10% or 12.5% taking effect July 24. As part of the announcement, Bangladesh, Indonesia, Cambodia, and Malaysia will receive tariff-rate quotas allowing certain textile and apparel imports to enter the U.S. without the new tariffs if they use U.S. cotton and textile inputs. While the provision offers some support for U.S. cotton, those countries are not among the largest importers of U.S. cotton, limiting the near-term impact. It also remains to be seen whether additional countries could be included in future announcements, which would provide a more meaningful boost to demand.

Supply and Demand Overview

- The latest Export Sales Report showed Upland sales of 51,300 bales, up from the previous week but still below the recent average. China was the largest buyer, followed by Vietnam, India, Bangladesh, and Mexico.

- Upland exports totaled 276,300 bales, with Vietnam once again leading shipments, followed by Pakistan, Turkey, India, and Bangladesh. While shipments improved from the previous week, the U.S. will still need to average roughly 355,000 bales per week over the remaining weeks of the marketing year to reach USDA’s current export forecast of 12.2 million bales, making that target increasingly difficult to achieve.

- Pima sales totaled 3,200 bales, led by India, while exports reached 8,000 bales with Vietnam and India accounting for the largest shipments.

The Seam®

- As of Friday afternoon, grower offers totaled 1,063 bales. No activity reported on the G2B platform this week.