August 10, 2026

The Week Ahead

Cotton heads into a busy week with Wednesday’s August WASDE at the center of attention, while crop conditions, inflation data, export demand, and outside markets could all add to volatility following last week’s rally.

- Wednesday’s August USDA supply and demand report will be the biggest cotton-specific event of the week. The August report will include USDA’s first state-by-state production estimates of the season, along with updated acreage and yield estimates. With concerns building around the Southwest crop and December futures coming off their highest close since mid-May, traders will be watching closely for any changes to U.S. production and ending stocks.

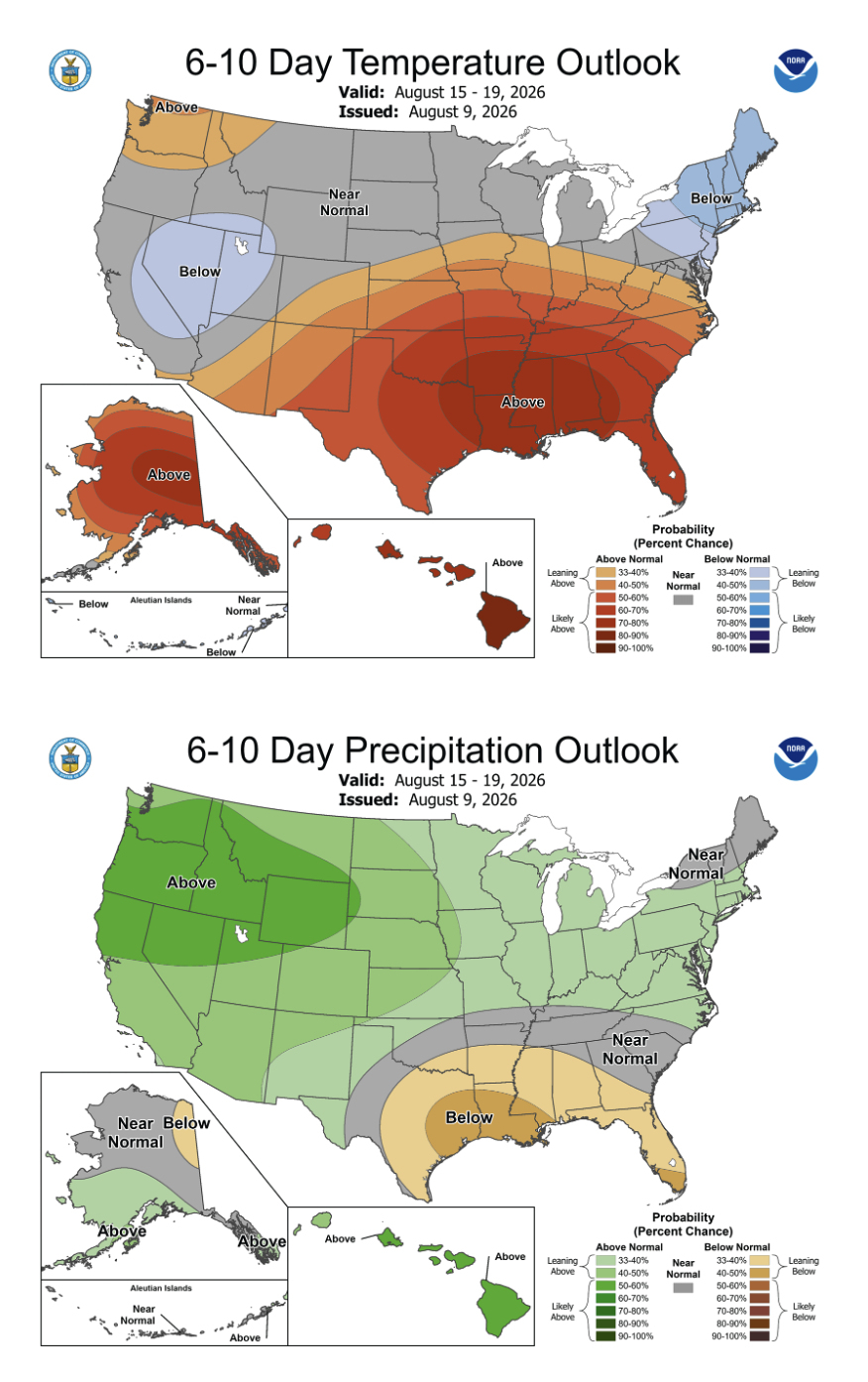

- Crop conditions and weather will also stay in focus ahead of the report. Monday’s Crop Progress report will provide another look at conditions after the national good-to-excellent rating fell last week, including another decline in Texas. Hot, dry weather is expected across much of the Southwest early this week, keeping stress on areas already short on moisture. With much of the crop moving through an important stage of development, August weather will be especially important for final yield potential.

- The macro calendar is packed, with CPI on Wednesday, PPI on Thursday, and retail sales on Friday. After last week’s weaker employment report pressured the dollar and helped commodities move higher, inflation will be the next major test for interest-rate expectations. A softer CPI print could add to that support, while hotter-than-expected inflation could strengthen the dollar and create a headwind for cotton.

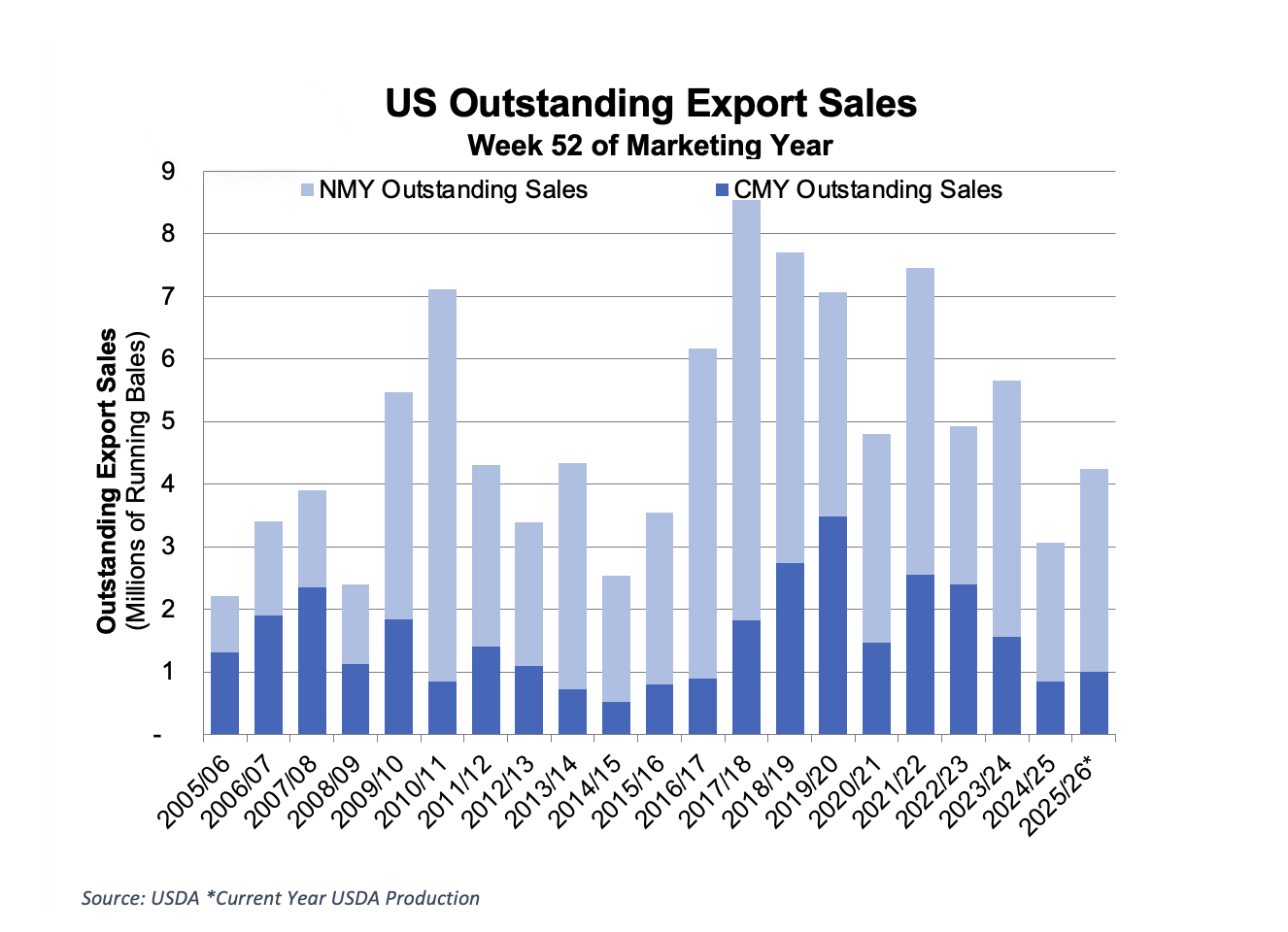

- Thursday’s Export Sales Report will give the first look at demand in the new marketing year. Attention will shift more fully toward 2026/27 commitments after solid new-crop buying in recent weeks. With futures now trading at higher levels, the pace of new business will be important to watch, particularly as cheaper Brazilian cotton competes for global demand.

- Outside markets could add another layer of volatility. U.S.-Iran negotiations over the Strait of Hormuz are still driving swings in crude oil, while the dollar will be sensitive to this week’s inflation and retail sales data. After outside markets helped cotton extend last week’s rally, shifts in either could have a larger influence if cotton-specific news is limited between Monday’s crop report and Wednesday’s WASDE.

Market Recap

- Cotton finished the week sharply higher, with December futures settling at 84.40 cents per pound, up 261 points on the week and at their highest level since mid-May. After struggling to get through 82 cents for several weeks, the market finally broke higher. December briefly traded below 81 cents Monday before reversing, and buying built from there as prices moved through several key technical levels.

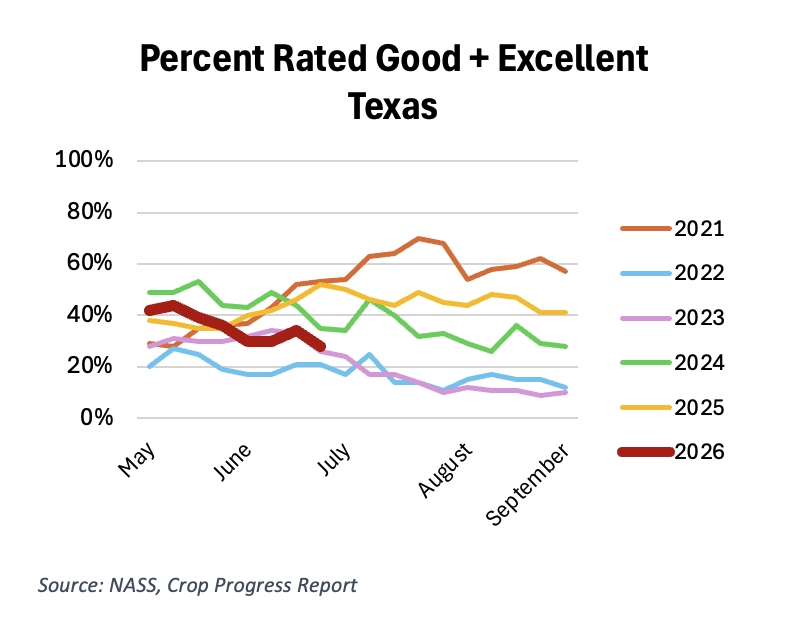

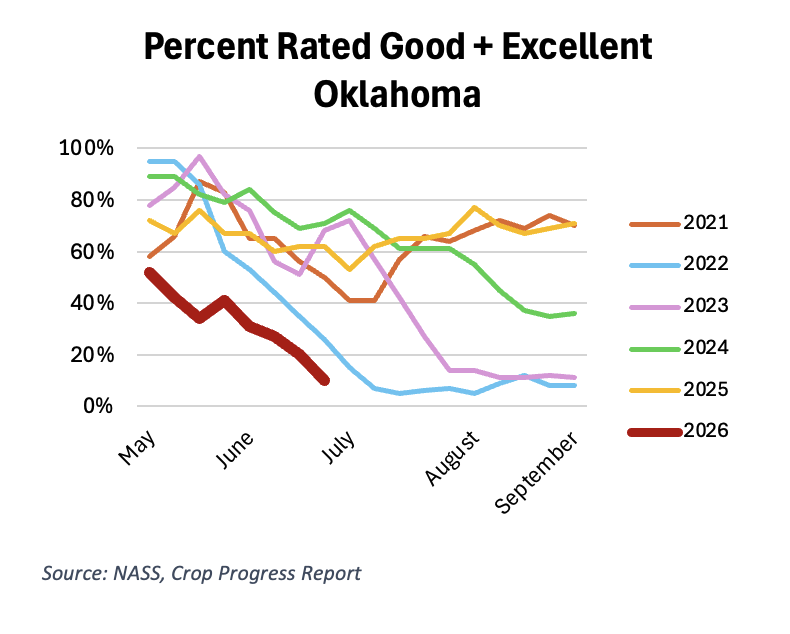

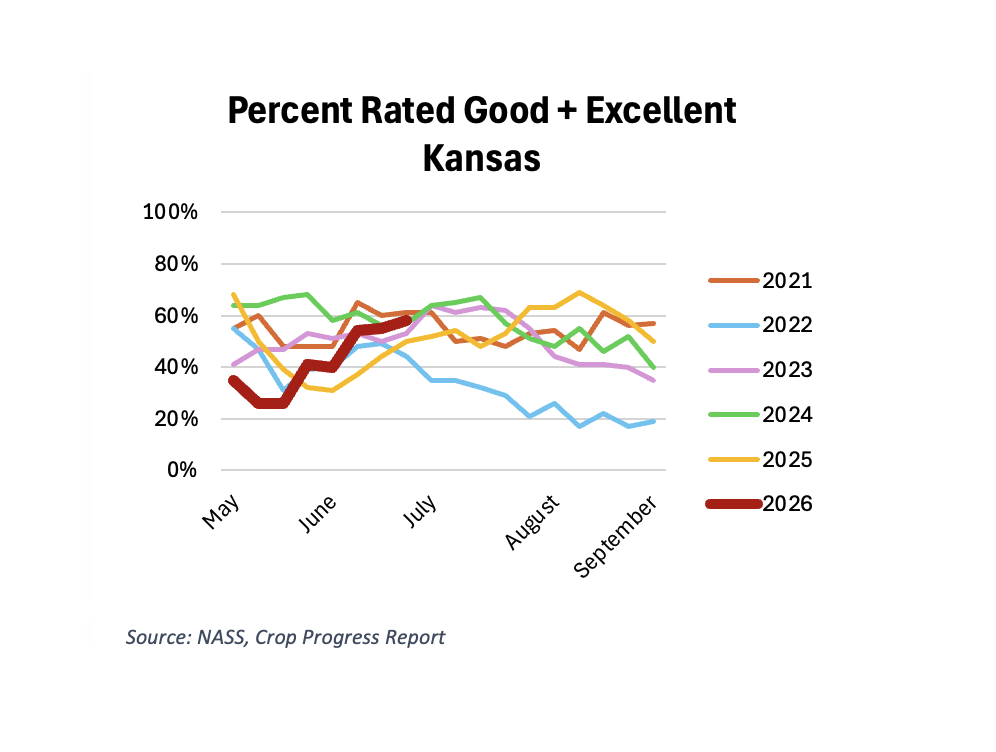

- Weather was also part of the story, with hot, dry conditions keeping crop concerns elevated throughout the week. Texas conditions slipped, with only 28% of the crop rated good to excellent, while Oklahoma fell to just 10%. Kansas was in better shape at 58%. Outside the U.S., weather concerns also picked up in China and India as crops move through an important stage of development.

- The first classing data of the season is starting to come in from South Texas, and early quality looks strong. While there is still plenty of crop left to class, South Texas is starting off close to where it left off last year.

- A good portion of last week’s move, though, came from fund and technical buying. Open interest increased by more than 15,000 contracts over the week as money moved into the market. Managed money added heavily to its net long position, while index funds were buyers again. With December finally pushing through resistance, that additional buying helped carry prices higher through the rest of the week.

- Friday brought another boost from outside markets. A weaker-than-expected U.S. jobs report shifted interest-rate expectations, pressured the dollar and helped commodities move higher. China also stayed in focus as reserve auctions sold out again and domestic cotton prices strengthened.

Economic and Policy Outlook

- The Senate left for August recess with several major legislative fights unresolved, including the SAVE America Act and another reconciliation package. The Senate Farm Bill also failed to advance out of committee, with disagreements over SNAP funding at the center of the dispute. Lawmakers return Sept. 14, leaving little time to reach a deal before the current Farm Bill extension expires Sept. 30. As a reminder, price supports for cotton and other commodities were enhanced through the One Big Beautiful Bill Act in July 2025 and are not affected by this portion of the Farm Bill.

- Iran said an agreement with Oman on shipping routes through the Strait of Hormuz is nearing completion, but reopening the waterway still depends on a broader agreement with the U.S. Tehran is seeking several concessions, including sanctions relief, compensation for U.S. strikes, an end to military threats and removal of the U.S. blockade. The U.S. has indicated it could lift the blockade once Iran follows through on its commitments, but the two sides are still communicating through intermediaries rather than negotiating directly. For now, uncertainty around a deal is keeping some risk premium in crude oil, with prices moving higher Monday after falling on reopening hopes last week.

- Last week’s weaker employment report shifted the macro picture in a more supportive direction for commodities. U.S. payrolls unexpectedly fell by 23,000 in July, while May and June were revised lower by a combined 103,000 jobs, raising concerns that the labor market is losing momentum and reducing expectations for a September rate hike. This week’s CPI and PPI reports will be the next test: softer inflation could keep pressure on the dollar and support commodities, while hotter readings could bring rate hike expectations back into focus. Friday’s retail sales report will also show whether weakness in the labor market is beginning to spill over into consumer spending.

Supply and Demand Overview

- The final full week of the 2025/26 marketing year showed Upland net reductions of 55,900 bales, a marketing-year low. Cancellations were led by Turkey and India, while China and Pakistan were among the few countries adding bales.

- New-crop sales were much stronger at 242,100 bales, led by Vietnam, Turkey, Honduras, India, and Pakistan.

- Upland exports totaled 222,800 bales, down 5% from the previous week and 7% from the four-week average. Vietnam was the largest destination, followed by Pakistan, Turkey, India, and Bangladesh. With the 2025/26 marketing year now wrapping up, attention will shift to final export totals and the pace of new-crop demand.

- Pima net reductions totaled 400 bales for 2025/26, while new-crop sales reached 8,300 bales, led primarily by India. Exports totaled 5,000 bales, up 11% from the previous week, with India accounting for most shipments.

The Seam®

As of Friday afternoon, grower offers totaled 4,306 bales. The past week 305 bales traded the G2B platform received an average price of 79.36 cents per pound. The average loan redemption rate (LRR) was 51.96, bringing the average premium over the LRR to 27.40 cents per pound.

Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).