As global economies recover from the coronavirus pandemic’s effects, many forecasts suggest there will be plenty of cotton to accommodate projected demand growth.

As global economies recover from the coronavirus pandemic’s effects, many forecasts suggest there will be plenty of cotton to accommodate projected demand growth.

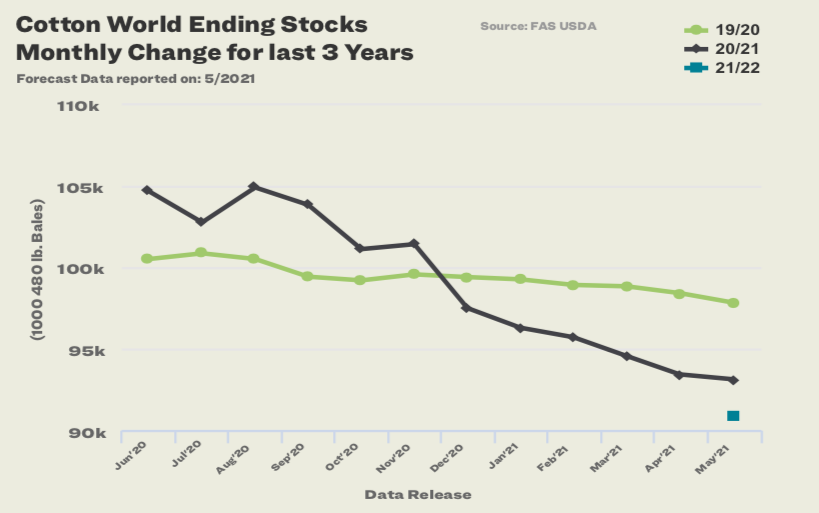

Market analysts use the stock-to-use ratio to measure the amount of cotton on hand at the end of the marketing year compared to the amount consumed. For 2020-21, USDA projects 79 percent while the 2021-22 estimate is 75 percent—both relatively high figures.

So why did prices rally so much this season? To answer this question, we need to look at the most desirable cottons’ location and availability.

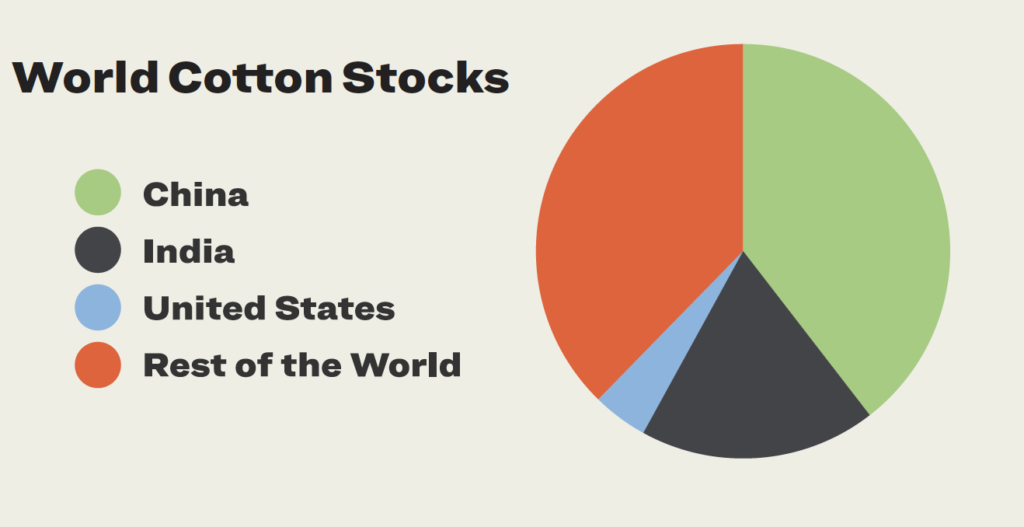

China and India hold considerable quantities of cotton. In both of these countries, government actors control most large stock “excesses.” In China, the National Strategic Reserve controls the timing and release of most cotton stocks. While heavy government supplies in China affected prices between 2011 and 2018, current Reserve activities have little impact on the market.

Similarly, the Cotton Corporation of India, which executes the government’s Minimum Support Price operations (purchasing seed cotton at a minimum level directly from farmers), auctions the cotton to the local and export markets. While India’s stocks are more loosely held than China’s, they are also not as available to the market as privately-owned cotton.

Outside of India and China, stocks are relatively tight, especially for the high-quality, machine-picked, contamination-free varieties (such as U.S. and Brazilian cotton). Considering that many consumers and governments are increasing scrutiny of textile sourcing, the demand for sustainable, responsibly-grown cotton has never been higher.

In May, USDA further reduced already tight ending stocks by lowering production estimates in both the U.S. and Brazil. Through week 40, 84 percent of available U.S. supplies have been sold, raising export commitments to more than 113 percent of this year’s production. Weekly export sales reports from the USDA Foreign Agricultural Service reveal continued robust sales as the pace of shipments has set new records. Given the robust export sales data, the USDA chose to increase their forecast for U.S. 2020-21 exports by 500,000 to 16.25 million statistical bales on the May WASDE report.

Combining the export analysis with planting intentions1, we continue to see a tight carryout for the next crop year. Most production estimates are considering substantial abandonment due to persistent drought in the southwest U.S. Should the moisture situation improve, we could see increases in both production and ending stocks. One scenario presented by the National Cotton Council estimated 2021-22 ending stocks in the U.S. below 3 million bales and a stock-to-use ratio of 14 percent. This level would likely support next year’s prices and provide some continuity with 2021 price trends.

It is also important that the USDA expects significantly lower production in Brazil during 2021 than in 2020. The current Brazilian crop had a difficult start with poor weather extending the planting season past the optimal growing season window.

It is also important that the USDA expects significantly lower production in Brazil during 2021 than in 2020. The current Brazilian crop had a difficult start with poor weather extending the planting season past the optimal growing season window.

When we consider all the fundamental data and combine it with potential speculative trader interest in cotton (along with other commodities), we see support for current prices along with the possibility of price appreciation should any production issues reduce next year’s supply. It’s also important to consider the amount of consumer discretionary money in circulation.

Considering the turbulence of the 2020-21 season, the longer-term outlook for cotton has a note of optimism. Cotton Incorporated expects global use to climb to 135-140 million bales by 2030 (a 15-20 percent increase over current levels) based on projections of world GDP growth. If Cotton Inc.’s expectations materialize, a bigger question will arise — “How do we continuously grow enough cotton to meet demand?” From where we see it, that would be a good problem to have.