Van May

The headlines above were taken out of various newspapers and industry publications over the last few weeks. They graphically demonstrate the difficult environment in which the entire U.S. textile industry currently operates.

I know you are aware how difficult things are on the farm. I want to be sure that you also are aware the U.S. textile industry is suffering at the same time. In fact, last year was the worst year in the history of the U.S. textile industry. The industry as a whole lost $300 million in the year 2000. You see it in those headlines. Plants are closing and 24,000 U.S. textile jobs were lost last year.

Our entire supply chain is sick from stem to stern, which impacts PCCA in several ways. First, the domestic textile industry has historically been U.S. cotton’s strongest, best, and most dependable customer. When it is in difficult times, it obviously impacts on its ability to use the cotton that you produce, and that is evident in today’s environment. In fact, over the past three years U.S. cotton consumption by the domestic textile industry has dropped from 11 million bales annually to the most recent annualized number of 8.6 million bales as of last month. That impact is easily seen in the horrible prices at which cotton is now trading.

Also, it means we have to keep a much closer eye on our accounts receivable as even the stronger companies who are still remaining as good, viable customers have suffered occasional cash flow difficulties during this period. We are on top of this one and, to date, have had no uncollectibles.

Finally, as a textile manufacturer ourselves, we are obviously feeling the results of this difficult market.

Not only is the industry struggling as a whole, but Levi Strauss and Co.’s business, in particular, has been poor as well. Their domestic presence is roughly one half of what it was three to four years ago. As you are aware, this forced us to move into the broader marketing chain and develop a larger and more diverse portfolio of customers. We have done that successfully and are very pleased with those results, but it has still had a chilling impact on all of us who supplied Levi for so long.

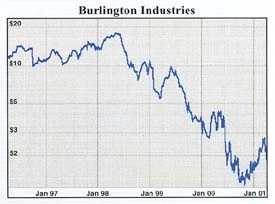

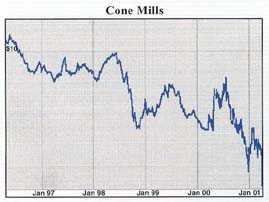

All Levi suppliers have been hammered by LS&Co.’s struggles. Look at these stock price charts for publicly traded industry giants Cone Mills and Burlington Industries, who, like us, counted on LS&Co. for most of their denim business.

Global price pressures on all of us in the denim business have taken most of the margin out of that business even when you can run your facilities full, as we currently are. As long as the dollar stays strong relative to other currencies around the world, I suspect this global price pressure on us will continue. Nonetheless, we are able to make a margin on our denim business currently, and that puts us in rare company in today’s textile environment. Denim continues to be a bright spot, just not as bright as it once was.

The story is a lot less pleasing in our yarn-dyed operation. That market has almost completely turned away from U.S. suppliers, and that is why we worked so hard to get Caribbean Basin legislation passed by Congress last year in hopes it would increase opportunities to recapture market share for those products in this hemisphere. Following Congressional approval of the legislation, we spent lots of time, travel, and energy in exploring those opportunities in Central America and the Caribbean Basin. Sadly, it does not appear those opportunities are realistic, and we are actively pursuing an alternative use of our yarn-dyed facilities, equipment, and personnel. By the time you read this, you may have already heard details of our plan. If not, we will share those details with you in the next issue of Commentator.

Actually, we have fared better than most in the business. As the industry was losing money last year, we actually posted a small profit in our textile operation. However, that will not be the case this year. We will certainly have a loss in the Textile Division when we close the books on June 30.

Suffice it to say that the past year and a half in the whole U.S. cotton/textile supply chain have been very challenging and very disappointing. Momma told me there would be days like this.

Van May